How To Budget Using The 50/20/30 Rule

Getting that first paycheck gives us that kind of rush that excites our consumerist behavior. We just want to spend it and bathe in our hard-earned money. We gratify ourselves for the long and tiring job that we are currently at. There is nothing wrong with celebrating once in a while, just make sure that you will not zero at your bank in one spending.

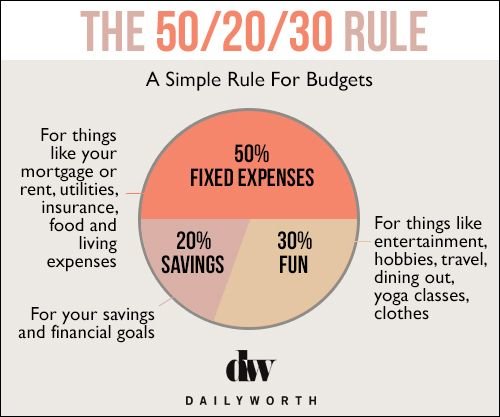

Illustration showing the 50/20/30 rule

Budgeting can be very overwhelming, especially to those who are beginners. People usually find themselves at crossroads of whether to shop or to save. Both can be done by the 50/20/30 rule of budgeting.

The 50/20/30 Rule

This rule will help us budget our money by categorizing our spending in three categories:

- 50% of that monthly salary should be placed in living essentials and food. This includes rent, utility fees, bills, and other necessities in your life. Transportation fees, either by commute or car maintenance and gasoline should also be included in the 50%

- 20% of our money should be set aside for some kind of financial goals. These include long and short-term savings. Some people will split this in half for the long-term, like retirement, and the other half is for short-term goals like paying off a debt. No matter what the financial goal is, it should always be 20% of the net income.

- While the 30% of the money should be placed for flexible things. This is where we should put in all our wants from clothes to travel. Spur of the moment plans like movie and dinner dates should also be charged here. It’s intentionally bigger than the savings part so that we don’t have any reasons for taking out funds from that 20%.

How to start the budget plan

In every budgeting plans, the first step is always the assessment part. It’s where we try to add in all our expenses and picture out the kind of lifestyle that we want. The next thing is to check your monthly earnings and try to weigh if our earnings are enough for all the things we are actually spending. If you find it enough for the necessities, yet you still find yourself without savings, then maybe because you are actually spending more on your wants. If this is the case, it’s time to make some cutbacks.

Make sure to fit all your wants in the 30% of your budget plan

The next thing you should do is to track your monetary activities down to the last dollar. You can tabulate it on a spreadsheet for easier access. Once you’ve been able to write down your spending for that period, try dividing those into three categories. This way, you can have a clear view on the things that belongs to your 50, 20, and 30.

When setting up for the 20%, make some realistic financial goals to avoid frustration. And if you currently have a debt to pay, never forget to put that in. The faster you pay it off, the bigger your savings will be.

Why use this method?

The good thing about this rule is that it adjusts to every person’s monthly income. It doesn’t force you on a specific amount unlike other methods. Because our salary will become the basis of this plan, we can have more control over it which means the more likely we commit to it.

Account every dollar you spend so you’ll know which areas to work on

It’s a very good layout to those who are just new in budgeting and don’t really have a clue on what to do. Also, unlike other budgeting methods, this one actually gives us a space to spend on our wants. Others get snub and will just advice to pay the bills, save, and invest. Let’s admit it, there’s no fun in that. With this rule, we can enjoy our money without feeling guilty since it’s already budgeted.

Bottomline:

There are many ways to budget our money, and this is not the only rule that guarantees good outcomes. It still depends on the person on what he/she wants to do with the money. For others, following this rule is a little bit constricting, especially to the family bread winners. But just like in everything else, the rule “it’s only difficult the first time” also applies to saving. The more we ease into it, the more we can realize that budgeting is really not that hard.

More in Advisor

-

`

Streaming Giant Netflix Faces Yet Another Challenge

Streaming Giant Netflix Faces Yet Another ChallengeIn the ever-evolving landscape of streaming entertainment, Netflix, once the unchallenged king of digital content, now faces a complex puzzle beyond...

December 1, 2023 -

`

Signs You Should Quit Your Current Job & Move On

Signs You Should Quit Your Current Job & Move OnYou Don’t Feel Comfortable at Work Imagine spending the majority of your waking hours in a place where you feel uneasy,...

November 20, 2023 -

`

How to Adjust and Renew Your Portfolio

How to Adjust and Renew Your PortfolioInvesting in the financial world is like navigating an ever-changing landscape—constantly evolving, always shifting. The key to staying on track? Regularly...

November 18, 2023 -

`

Dr. Dre’s Divorce With Nicole Young: A Closer Look

Dr. Dre’s Divorce With Nicole Young: A Closer LookWhen the beats of old-school hip-hop start bumping, Dr. Dre’s name reverberates in fans’ minds worldwide. Born as Andre Young, this...

November 12, 2023 -

`

Why Branded Content Is the Best Way to Connect With Your Audience

Why Branded Content Is the Best Way to Connect With Your AudienceHave you ever found yourself deep in a compelling article or engrossed in a video series, only to later discover that...

November 5, 2023 -

`

Why the Gender Pay Gap Could Be Getting Worse | New Research Findings

Why the Gender Pay Gap Could Be Getting Worse | New Research FindingsAt a time when women are making significant strides in various professional arenas, a new report throws light on a trend...

October 28, 2023 -

`

What Is a Bull Market and How Can Investors Benefit From One?

What Is a Bull Market and How Can Investors Benefit From One?In finance, the term “bull market” is frequently used to describe a period of optimism, rising asset prices, and investor confidence....

October 19, 2023 -

`

A-List Power Couples Where the Women Make More Money

A-List Power Couples Where the Women Make More MoneyIn an era of shifting gender roles and evolving definitions of success, it’s increasingly common to find celebrity couples where the...

October 15, 2023 -

`

Massive Price Cuts: Tesla Only Witnesses ‘Modest’ Sales Gain in China

Massive Price Cuts: Tesla Only Witnesses ‘Modest’ Sales Gain in ChinaCutting Down Prices, But Not Cutting the Mustard? Summer 2023 brought with it a promise of sunshine and relaxation. For Tesla...

October 8, 2023

More From InvestmentGuru

-

The Transformation of Jeff Bezos’ Eye: Analyzing Changes

The Transformation of Jeff Bezos’ Eye: Analyzing ChangesJeff Bezos, the iconic founder of Amazon and a pivotal figure in global commerce, has long been under the scrutinizing lens...

Rich & FamousApril 14, 2024 -

7 Practical Ways to Figure Out the Career You Actually Want

7 Practical Ways to Figure Out the Career You Actually WantHow to figure out what career you want? Well, it can often feel like trying to solve a complex puzzle with...

AdvisorApril 12, 2024 -

Everything You Ought to Know About Land Loans

Everything You Ought to Know About Land LoansIf you are looking to buy a new property in 2024, you need to understand land loans. Specifically, land loan interest...

InvestmentsApril 5, 2024 -

Is Spirit Airlines Safe? Here’s Your Ultimate Guide

Is Spirit Airlines Safe? Here’s Your Ultimate GuideBefore you book your next flight, it is perfectly normal to ponder, “Is Spirit Airlines safe?” With its reputation for being...

BusinessMarch 28, 2024 -

Olivia Colman Confesses to Using Cosmetic Injections

Olivia Colman Confesses to Using Cosmetic InjectionsEnglish actress Olivia Colman recently made headlines not for a new role or award but for her openness about cosmetic injections....

Rich & FamousMarch 24, 2024

You must be logged in to post a comment Login