3 Months of Living Expenses Isn’t Enough to Fund Your Emergency Account, Expert Says

Orman rejects 3-6 months minimum

It is a universal consensus among financial experts that the minimum one needs to have in an emergency account is the living expenses required for 3-6 months. However, Suze Orman, a financial expert and a onetime CNBC television host, has a divergent opinion.

While addressing a question at the 2017 emerge Americas conference on the appropriate amount to have in an emergency fund, Orman stated that those who hold such opinion that 3-6 months worth of living expenses is the ideal minimum range are not realistic. Orman expressly said that 3-6 months worth of living expenses is nowhere near sufficient to provide financial security.

Orman opined that people who believe that 3-6months living expenses are enough to fund an emergency account are wrong

The financial expert raised several issues and painted several scenarios to drive home her point. One of such questions was inquiring into what the audience felt will happen if they lose their current jobs and remain unemployed for a whole year or encounter unforeseen medical emergencies.

Orman stressed her point that different unforeseen incidents could happen which would take away all savings and she thus concluded that it is more advisable to have a minimum of eight to twelve months worth of living expenses in an emergency fund. She further emphasized that one needs to be assured of his/her security when such unforeseen circumstances come up.

Orman suggests 8-12 months minimum

While still addressing the participants at the conference, Orman called to the remembrance of the audience their situations during the financial chaos in 2007 caused by the Great Recession. She reminded them that a lot of people lost their jobs and everything they had. Orman added that there were some of them who had gotten involved in tech start-ups but the recession caused their start-ups to fail.

She further mentioned that the sole reason why those things happened was the fact that people didn’t have spare capital to use as an investment and no one was interested in IPO since the market value kept declining and there was nothing to do. She further reminded them that it took several people more than three to six months to get employment after the great recession.

Orman emphatically stated that the issue goes beyond the economy as sickness, accident or any crazy occurrence can arise, and the only way to handle any such incident is to secure one’s self. She noted that the only way to ensure true financial security at all times is to have a formidable emergency fund built up with a minimum of eight to twelve months cost of living expenses. Reiterating her previous points, Orman finally noted that there is a need to have enough money in one’s bank account to attain this security and no one should be dependent on a credit card.

Orman mentioned that to build a minimum of eight to twelve months living expenses is needed to establish a robust emergency fund

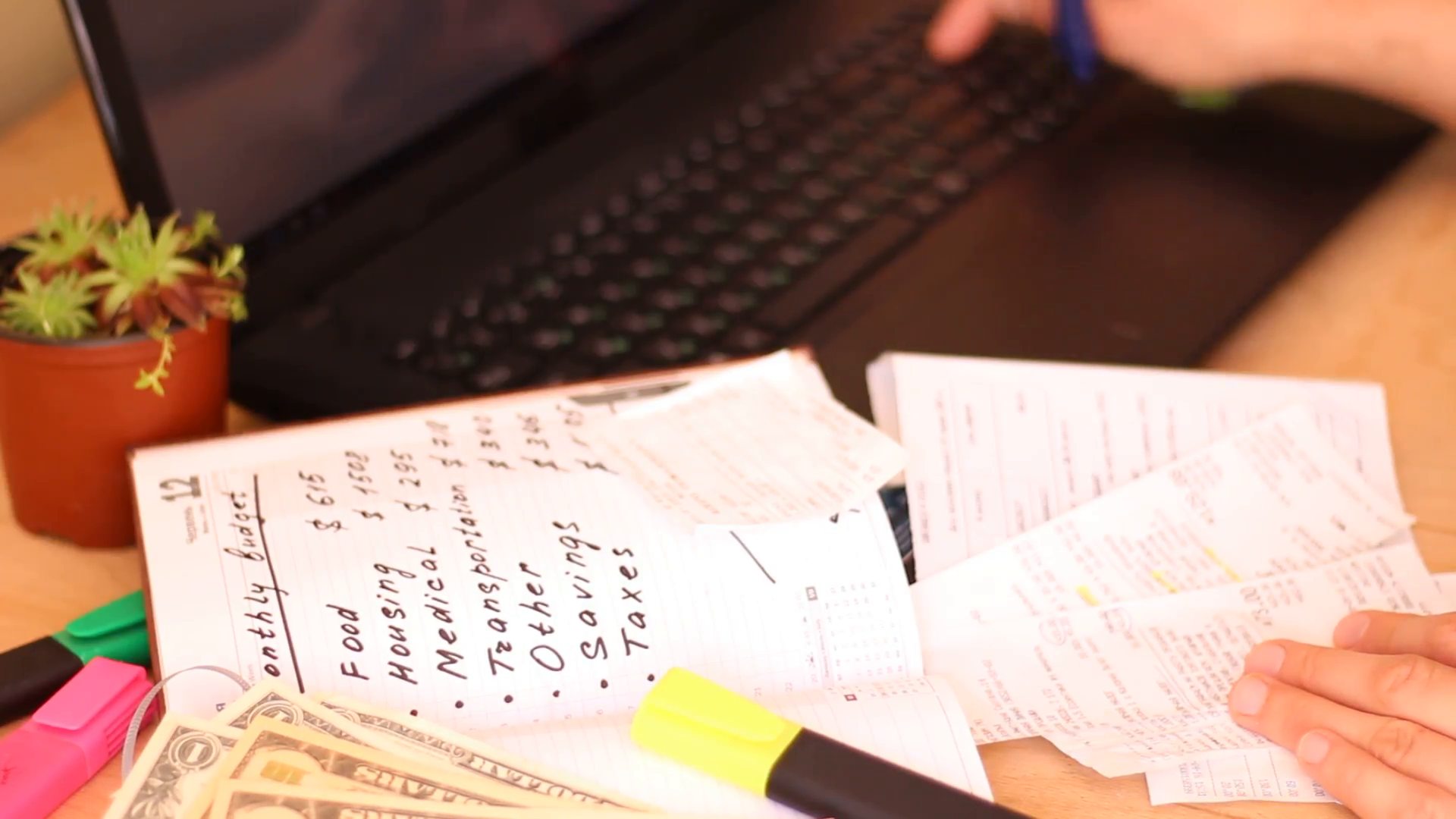

How to increase savings

Based on Orman’s suggestions, media outlets have highlighted that a recently conducted survey indicates that only 39 percent of Americans have sufficient funds to cover an emergency of about $1,000. This result suggests that a lot of Americans still have insufficient emergency funds.

Experts have suggested that different things that can be done to build up this fund. One of such is a budget re-evaluation and making stern decisions about what portion of a budget to use as additional savings or investment. Experts maintain that it is best to put away money very early to enjoy all the benefits and advantages accruing to compound interest. Compound interest directly implies that a little sum invested will end up becoming a whole lot of money sometimes later.

One way to cut out expenses and increase savings is by cutting out convenience such as taking taxis every day.

A media outlet records that there are different viable ways to plan a budget and still have enough to put away in an emergency fund. One of such techniques is by tracking expenses to determine costs and ultimately detecting what all the money made is being used for.

Expense tracking requires that you record all purchases made. One other means closely similar to expense tracking is writing out a list before you go shopping so you know just exactly what you need and you do not end up spending on unnecessary items.

Another exciting method developed by David, the founder of Zero Days Finance is to select a day of the week where you do not spend money on anything at all including coffee and groceries. One other way to increase savings is by cutting out convenience such as placing orders for takeouts and taking taxis regularly.

More in Advisor

-

`

Celebrity Couples Who Have Ended Their Relationships in 2025

Celebrity Couples Who Have Ended Their Relationships in 20252025 has already seen its fair share of celebrity breakups, and the year is just getting started. From heartfelt announcements to...

February 6, 2025 -

`

How Trump’s Policies Will Reshape Artificial Intelligence in the U.S.

How Trump’s Policies Will Reshape Artificial Intelligence in the U.S.The United States witnessed a significant political shift as Donald Trump took the presidential oath once again. His return to the...

January 31, 2025 -

`

Millie Bobby Brown Shuts Down Age-Shamers with a Powerful Message

Millie Bobby Brown Shuts Down Age-Shamers with a Powerful MessageFrom the moment Millie Bobby Brown first appeared as Eleven in “Stranger Things,” she captured hearts worldwide. But growing up in...

January 25, 2025 -

`

Why Outsourcing Payroll Services Is a Smart Business Move

Why Outsourcing Payroll Services Is a Smart Business MoveManaging payroll is no small task—it’s a crucial part of any business that ensures employees are paid accurately and on time....

January 15, 2025 -

`

These AI Stocks Should Be on the Watch List of Investors in 2025

These AI Stocks Should Be on the Watch List of Investors in 2025The buzz around AI stocks is growing louder than ever. With artificial intelligence shaping industries like healthcare, finance, and tech, smart...

January 8, 2025 -

`

Why the Starbucks Workers Strike Is Expanding Across U.S. Cities

Why the Starbucks Workers Strike Is Expanding Across U.S. CitiesThe Starbucks workers’ strike has gained significant momentum, with employees in more U.S. cities joining the movement to address unresolved issues...

January 2, 2025 -

`

Are Shawn Mendes and Camila Cabello Still Close After Breakup?

Are Shawn Mendes and Camila Cabello Still Close After Breakup?The connection between Shawn Mendes and Camila Cabello continues to intrigue fans worldwide. Their shared history, from chart-topping collaborations to a...

December 24, 2024 -

`

Here’s What It Takes to Become a Professional Physical Therapist

Here’s What It Takes to Become a Professional Physical TherapistPhysical therapy is a career that blends science, empathy, and problem-solving to help people recover from injuries or improve mobility. Knowing...

December 19, 2024 -

`

GM Battery Cell Plant Deal Marks $1 Billion Ownership Shift

GM Battery Cell Plant Deal Marks $1 Billion Ownership ShiftGeneral Motors (GM) plans to sell its stake in a $2.6 billion electric vehicle battery cell plant in Lansing, Michigan. This...

December 11, 2024

More From InvestmentGuru

-

What Are Personal Loans Used For? 7 Reasons That Make Sense

What Are Personal Loans Used For? 7 Reasons That Make SenseWhen unexpected expenses arise or planned costs stretch the budget, a personal loan offers a reliable financial option. Unlike credit cards,...

AdvisorJune 26, 2025 -

Top 5 Stocks Under $5 That Could See Big Gains in the Long Run

Top 5 Stocks Under $5 That Could See Big Gains in the Long RunNot all great investments wear a big price tag. Some of the most promising opportunities lie with stocks priced under $5...

InvestmentsJune 19, 2025 -

Trump Gets Grilled Online as ‘TACO Trump’ Memes Go Viral

Trump Gets Grilled Online as ‘TACO Trump’ Memes Go ViralMemes are having a field day, and this time, the internet has turned its lens to President Donald Trump. Across X,...

BusinessJune 12, 2025 -

8 Celebrities Who Love Costco Just as Much as You Do

8 Celebrities Who Love Costco Just as Much as You DoCostco may be known for its bulk deals and iconic $1.50 hot dog combo, but it’s not just everyday shoppers who...

Rich & FamousJune 6, 2025 -

14 Business Leaders Share Career Advice That Still Guides Them

14 Business Leaders Share Career Advice That Still Guides ThemWe all start somewhere. And for many successful business leaders, it was a few words of advice early in their careers...

AdvisorMay 29, 2025

You must be logged in to post a comment Login