Finances Got You By The Throat? Here’s How You Can Reduce Your Tax Payments This Year

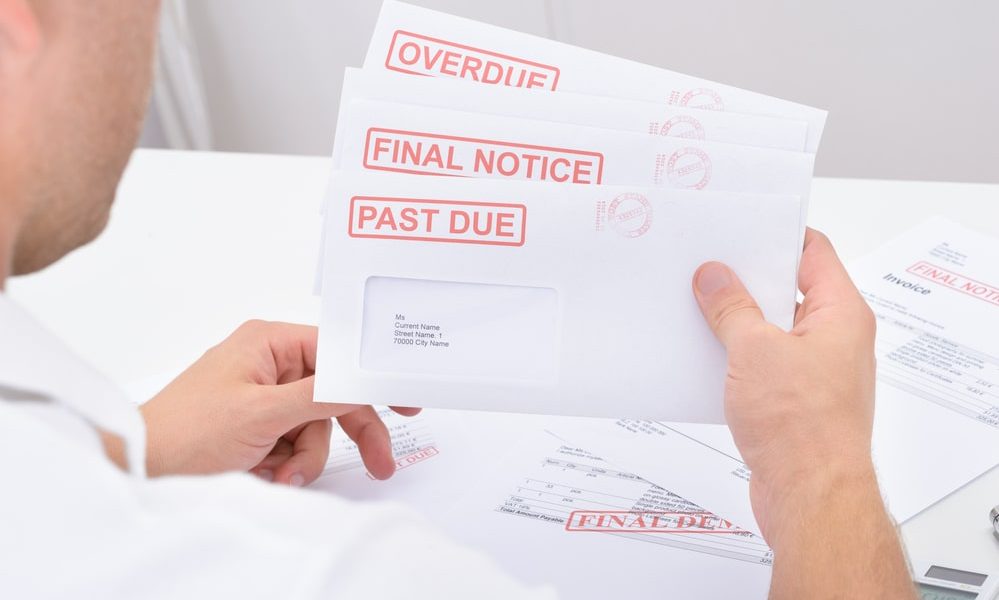

Tax day is due July 15th and not everyone is looking forward to it. In 2019, approximately 8 million people did not pay their taxes. On top of that, the stress as a result of the COVID-19 pandemic is putting the economic system into uncertainty- so much so, that in 2020, 37% of taxpayers said that they do not have the resources to pay this year’s taxes.

However, to aid taxpayers, the federal government did give an extra 90 days to close the payments this year since the original date was April 15th. But, what if you are still unable to pay them? Is there any hope for you?

Deposit Photos | Paying taxes this year is difficult for many people around the country

We’re here to offer some guidance. The first thing to do is not panic. Instead, try to understand that many people from all walks of life face this situation in their lifetime. For those currently in the fold, there are various options available to help taxpayers out:

1. Monthly Installment plan

If you are behind payments but not by a considerable amount, opting for an installment plan might be your smartest move. What you need to do is file your return, log in to irs.gov and fill out the online payment agreement application.

For monthly installments, you can download Form 9465, which will give you 72 months to complete the payment. However, this is for payments equal to or less than $50,000, including interest, tax, and penalties.

Moreover, you need to be eligible for the program with previous tax returns filed first. Lastly, business owners and self-employed people with quarterly payments would have to make payments in the current year so they meet their deadlines.

Deposit Photos | Eligibility for form 9465 requires an amount of $50,000 or less

2. Request an Offer to Clear Payments

This is option two for taxpayers who simply do not have the resources to pay back what they owe. It is really a gamble in which you make an offer to the IRS, and if it’s accepted, that’s the total you have to pay. In layman terms, it’s the IRS asking you how much you have on you and making a compromise. As a result, you don’t have to pay the full amount. However, some different terms and conditions need to be met for payments to be accepted.

For instance, the IRS will check your income, expenses, asset equity, and ability to pay to determine whether you’re really going all-in with the offer made. If yes, then they will most likely approve it. There are some risks involved in doing this. First, you have to pay 20% upfront and the rest in installments. If you fail to pay the installments, chances are the IRS might sue you for the original amount along with interest and penalties.

Deposit Photos | Take a chance and meet with the IRS to discuss a probable reduction in payments

3. Partial Payments and Complete Paperwork

The most important thing you must do is to file your tax returns regardless of whether or not you have the payments. Filing could save you from a lot of trouble in the future. Secondly, if you are unable to pay in full, try to pay a small amount at least every month. What this does is at least prove your intent to pay even if it’s not in full. Plus, you get to save yourself from punishing penalties. Failure to file is worse than not paying the taxes.

More in Advisor

-

`

The Push for Tax-Free Tips in America – A Win or a Risk?

The Push for Tax-Free Tips in America – A Win or a Risk?Tipping has long been a fundamental part of the American service industry, providing essential income for millions of workers. However, the...

February 20, 2025 -

`

Matthew Perry Foundation Launches Addiction Fellowship at MGH

Matthew Perry Foundation Launches Addiction Fellowship at MGHThe impact of addiction on individuals and families is profound, and the need for specialized medical care in this field has...

February 13, 2025 -

`

Celebrity Couples Who Have Ended Their Relationships in 2025

Celebrity Couples Who Have Ended Their Relationships in 20252025 has already seen its fair share of celebrity breakups, and the year is just getting started. From heartfelt announcements to...

February 6, 2025 -

`

How Trump’s Policies Will Reshape Artificial Intelligence in the U.S.

How Trump’s Policies Will Reshape Artificial Intelligence in the U.S.The United States witnessed a significant political shift as Donald Trump took the presidential oath once again. His return to the...

January 31, 2025 -

`

Millie Bobby Brown Shuts Down Age-Shamers with a Powerful Message

Millie Bobby Brown Shuts Down Age-Shamers with a Powerful MessageFrom the moment Millie Bobby Brown first appeared as Eleven in “Stranger Things,” she captured hearts worldwide. But growing up in...

January 25, 2025 -

`

Why Outsourcing Payroll Services Is a Smart Business Move

Why Outsourcing Payroll Services Is a Smart Business MoveManaging payroll is no small task—it’s a crucial part of any business that ensures employees are paid accurately and on time....

January 15, 2025 -

`

These AI Stocks Should Be on the Watch List of Investors in 2025

These AI Stocks Should Be on the Watch List of Investors in 2025The buzz around AI stocks is growing louder than ever. With artificial intelligence shaping industries like healthcare, finance, and tech, smart...

January 8, 2025 -

`

Why the Starbucks Workers Strike Is Expanding Across U.S. Cities

Why the Starbucks Workers Strike Is Expanding Across U.S. CitiesThe Starbucks workers’ strike has gained significant momentum, with employees in more U.S. cities joining the movement to address unresolved issues...

January 2, 2025 -

`

Are Shawn Mendes and Camila Cabello Still Close After Breakup?

Are Shawn Mendes and Camila Cabello Still Close After Breakup?The connection between Shawn Mendes and Camila Cabello continues to intrigue fans worldwide. Their shared history, from chart-topping collaborations to a...

December 24, 2024

More From InvestmentGuru

-

Donald Trump’s Billion-Dollar Business Empire Explained

Donald Trump’s Billion-Dollar Business Empire ExplainedDonald Trump’s income streams are as layered as his public persona. While many still associate his fortune with towering buildings and...

BusinessJuly 10, 2025 -

Why So Many Celebrities Are Launching Their Own Mobile Networks

Why So Many Celebrities Are Launching Their Own Mobile NetworksMobile phone carriers used to be the domain of massive telecom corporations. But recently, a curious shift has taken place: celebrities...

Rich & FamousJuly 4, 2025 -

What Are Personal Loans Used For? 7 Reasons That Make Sense

What Are Personal Loans Used For? 7 Reasons That Make SenseWhen unexpected expenses arise or planned costs stretch the budget, a personal loan offers a reliable financial option. Unlike credit cards,...

AdvisorJune 26, 2025 -

Top 5 Stocks Under $5 That Could See Big Gains in the Long Run

Top 5 Stocks Under $5 That Could See Big Gains in the Long RunNot all great investments wear a big price tag. Some of the most promising opportunities lie with stocks priced under $5...

InvestmentsJune 19, 2025 -

Trump Gets Grilled Online as ‘TACO Trump’ Memes Go Viral

Trump Gets Grilled Online as ‘TACO Trump’ Memes Go ViralMemes are having a field day, and this time, the internet has turned its lens to President Donald Trump. Across X,...

BusinessJune 12, 2025

You must be logged in to post a comment Login