How To Budget Using The 50/20/30 Rule

Getting that first paycheck gives us that kind of rush that excites our consumerist behavior. We just want to spend it and bathe in our hard-earned money. We gratify ourselves for the long and tiring job that we are currently at. There is nothing wrong with celebrating once in a while, just make sure that you will not zero at your bank in one spending.

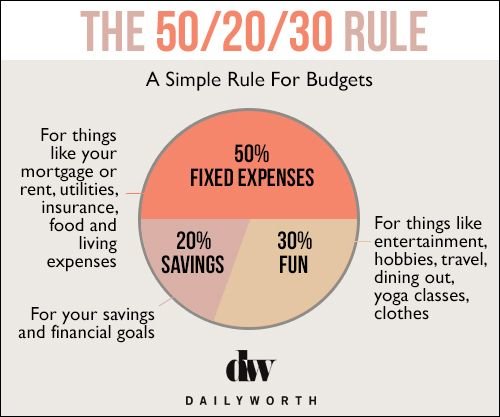

Illustration showing the 50/20/30 rule

Budgeting can be very overwhelming, especially to those who are beginners. People usually find themselves at crossroads of whether to shop or to save. Both can be done by the 50/20/30 rule of budgeting.

The 50/20/30 Rule

This rule will help us budget our money by categorizing our spending in three categories:

- 50% of that monthly salary should be placed in living essentials and food. This includes rent, utility fees, bills, and other necessities in your life. Transportation fees, either by commute or car maintenance and gasoline should also be included in the 50%

- 20% of our money should be set aside for some kind of financial goals. These include long and short-term savings. Some people will split this in half for the long-term, like retirement, and the other half is for short-term goals like paying off a debt. No matter what the financial goal is, it should always be 20% of the net income.

- While the 30% of the money should be placed for flexible things. This is where we should put in all our wants from clothes to travel. Spur of the moment plans like movie and dinner dates should also be charged here. It’s intentionally bigger than the savings part so that we don’t have any reasons for taking out funds from that 20%.

How to start the budget plan

In every budgeting plans, the first step is always the assessment part. It’s where we try to add in all our expenses and picture out the kind of lifestyle that we want. The next thing is to check your monthly earnings and try to weigh if our earnings are enough for all the things we are actually spending. If you find it enough for the necessities, yet you still find yourself without savings, then maybe because you are actually spending more on your wants. If this is the case, it’s time to make some cutbacks.

Make sure to fit all your wants in the 30% of your budget plan

The next thing you should do is to track your monetary activities down to the last dollar. You can tabulate it on a spreadsheet for easier access. Once you’ve been able to write down your spending for that period, try dividing those into three categories. This way, you can have a clear view on the things that belongs to your 50, 20, and 30.

When setting up for the 20%, make some realistic financial goals to avoid frustration. And if you currently have a debt to pay, never forget to put that in. The faster you pay it off, the bigger your savings will be.

Why use this method?

The good thing about this rule is that it adjusts to every person’s monthly income. It doesn’t force you on a specific amount unlike other methods. Because our salary will become the basis of this plan, we can have more control over it which means the more likely we commit to it.

Account every dollar you spend so you’ll know which areas to work on

It’s a very good layout to those who are just new in budgeting and don’t really have a clue on what to do. Also, unlike other budgeting methods, this one actually gives us a space to spend on our wants. Others get snub and will just advice to pay the bills, save, and invest. Let’s admit it, there’s no fun in that. With this rule, we can enjoy our money without feeling guilty since it’s already budgeted.

Bottomline:

There are many ways to budget our money, and this is not the only rule that guarantees good outcomes. It still depends on the person on what he/she wants to do with the money. For others, following this rule is a little bit constricting, especially to the family bread winners. But just like in everything else, the rule “it’s only difficult the first time” also applies to saving. The more we ease into it, the more we can realize that budgeting is really not that hard.

More in Advisor

-

`

The Growing Relevance of Investment Governance in Retail Advice

The Growing Relevance of Investment Governance in Retail AdviceInvestment governance, once the domain of large institutions, now stands as a cornerstone of retail financial advice. As model portfolio services...

November 9, 2025 -

`

5 Reasons Why Montenegro is Europe’s Newest Luxury Hotspot

5 Reasons Why Montenegro is Europe’s Newest Luxury HotspotOnce a hush-hush escape for the well-connected, Montenegro is stepping into the spotlight. Tucked along the Adriatic Sea, it is attracting...

November 9, 2025 -

`

How to Spot Real Investment Gems in the Travel Industry

How to Spot Real Investment Gems in the Travel IndustryThe global travel industry continues to evolve at lightning speed, creating one of the most powerful investment landscapes on the planet....

November 2, 2025 -

`

How to Invest in REMX, Rare Earth Supply Chain

How to Invest in REMX, Rare Earth Supply ChainREMX isn’t your typical ETF. It doesn’t track broad markets or play it safe. It is a high-conviction bet on the...

October 31, 2025 -

`

Top Strategies to Use Instagram DMs to Grow Your Business

Top Strategies to Use Instagram DMs to Grow Your BusinessInstagram has transformed into a hub where creativity meets commerce. Today, brands, creators, and entrepreneurs use it not only to post...

October 26, 2025 -

`

Master This Key ROI Formula for Smart Investment Decisions

Master This Key ROI Formula for Smart Investment DecisionsEvery smart investment starts with a clear view of what you are getting back. That is where return on investment (ROI)...

October 24, 2025 -

`

Comparing “The Life of a Showgirl” to Taylor Swift’s Other Albums

Comparing “The Life of a Showgirl” to Taylor Swift’s Other AlbumsTaylor Swift has spent nearly two decades redefining pop, country, and storytelling through music. With each era, she reinvents herself while...

October 19, 2025 -

`

How Do Your Retirement Savings Compare to Older Generations’?

How Do Your Retirement Savings Compare to Older Generations’?Retirement is a big milestone, but most people don’t know if they are saving enough to get there. For baby boomers,...

October 17, 2025 -

`

Will Bitcoin Crash to $0 or Hit $500K in a Decade?

Will Bitcoin Crash to $0 or Hit $500K in a Decade?Bitcoin’s future divides analysts into two extreme camps. Some see it becoming one of the most valuable financial assets in history....

October 12, 2025

More From InvestmentGuru

-

Why There Were No “Good Looks” at This Year’s Bezos Bash Met Gala

Why There Were No “Good Looks” at This Year’s Bezos Bash Met GalaThe Met Gala has always lived at the intersection of fashion, fame, and financial excess. This year, that intersection turned sharper....

Rich & FamousMay 24, 2026 -

Why the Ultra-Wealthy Are Investing Outside the US

Why the Ultra-Wealthy Are Investing Outside the USThe United States still holds its position as the world’s largest center for billionaire and millionaire wealth. Yet a noticeable shift...

AdvisorMay 17, 2026 -

SpaceX Is Going Public — Here’s What $5,000 Could Become in 5 Years

SpaceX Is Going Public — Here’s What $5,000 Could Become in 5 YearsAnticipation is building around one of the most closely watched public offerings in recent memory. SpaceX, led by Elon Musk, has...

InvestmentsMay 10, 2026 -

Reed Hastings, Netflix Co-Founder, Is Leaving the Company

Reed Hastings, Netflix Co-Founder, Is Leaving the CompanyNetflix confirmed in its first-quarter earnings report that Hastings will not seek reelection to the board and will officially part ways...

BusinessMay 1, 2026 -

Why the Rich and Famous Are Selling Their Ski Mansions in Secret

Why the Rich and Famous Are Selling Their Ski Mansions in SecretA quiet layer of Colorado’s ski-home market rarely shows up on public real estate platforms. Behind the scenes, multi-million-dollar mansions change...

Rich & FamousApril 25, 2026

You must be logged in to post a comment Login